Now that we’ve eliminated the risk to your principle, guaranteed never to lose money, and we’re participating in much higher market gains, let’s talk about fees.

Fees:

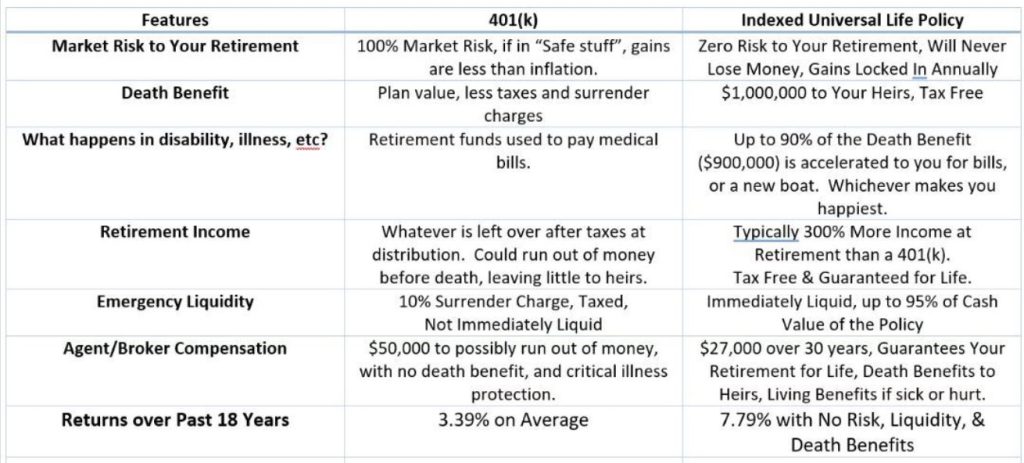

What is your 401(k) charging you in fees? Do you know? Have you investigated it? This is pretty important for the growth of your money, especially since this money will be taxed in the future. I can tell you on average, that 401(k) TOTAL fees, including all of the hidden fees in mutual funds, etc, average around 3% per year. Now, remember, the S&P 500 has only averaged a 3.39% Actual Rate of Return over the past 18 years….and let’s also remember that 89% of financial advisors cannot beat the S&P year to year. IUL policies are indexed TO the S&P or another index. Therefore, they go up with the index goes up, but don’t get down when it goes down.

What are the fees covering? They are buying you the expertise of those managing your money. That’s it. If you get sick, you get your money back after tax to pay your medical copay. If you die, your heirs get your money, after it’s been beaten to death with taxes.

What do fees cover with an IUL? The cost of insurance. Remember, we do not sell these solely as a safe place to put your money that will gain 100% of the market upside, with 0% of the downside. This is also an insurance policy with a death benefit, should it be required. If I were to hand your spouse a check for $1 million dollars, that costs money to provide that coverage. If I were to hand YOU a check for 90% of the death benefit, in the event of illness…that coverage costs money. However, your death benefit amount will always, 100% of the time, be worth more than the money you put into it, and it’s tax-free. Can your financial advisor say the same?

IUL has fees, and in total, they will be pretty close to the fees of a financial advisor for over 30 years. However, we offer you liquidity, safety, upside gains that are at least double that of the S&P over the past 18 years.

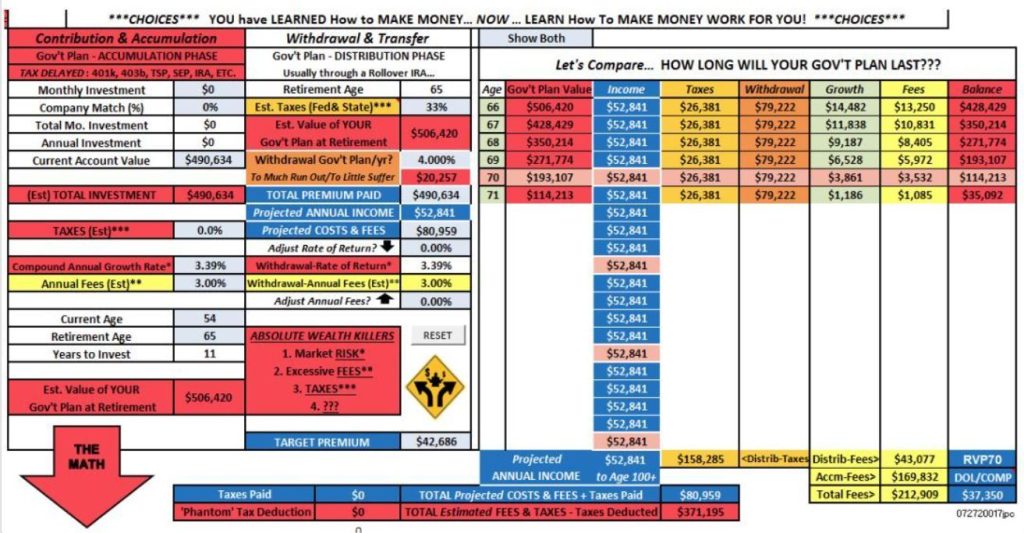

In the illustration below, the client has $490,634 in assets in a typical money management account. His government 401(k) plan grows to an estimated $506,420 at retirement.

We illustrated apples to apples with what our IUL will do for him, vs his managed, risk-based, account. We were able to project $52,841 in income, until age 120.

All things being equal, using his government-backed 401(k) plan, he’s out of money at age 71.

(fees illustrated until age 80 for IUL, and until runs out of money for 401(k)

Total Fees for 401(k) at 3%: $212,909 (no death benefit)

Total Fees for an IUL with a $1.4 million Death Benefit: $80,959

(btw, with our IUL death benefit, if he gets sick we’ll give him a check for up to $1,260,000 tax-free)

In most illustrations, we can get you more income at retirement than your financial advisor can, and you will never run out of money. When they try to match the income we can provide our clients with a properly structured, the client runs out of money by their mid-seventies. They CANNOT match us on income, on the death benefit, on living benefits (up to 90% of the death benefit), or a tax-free retirement until age 120.